1. Calculate your profit before you purchase the home.

The old saying is “you make your profit when you purchase the home not when you sell it”. This means calculating a profit and lost analysis on the Fix & Flip project before you purchase. Determine the profit before you purchase – work backwards. Don’t do a project unless there is a clear profit potential. Calculate your profit/Loss. Sales price less costs is your profit.

The old saying is “you make your profit when you purchase the home not when you sell it”. This means calculating a profit and lost analysis on the Fix & Flip project before you purchase. Determine the profit before you purchase – work backwards. Don’t do a project unless there is a clear profit potential. Calculate your profit/Loss. Sales price less costs is your profit.

1. Costs for Fix & Flip

- Acquisition

- Purchase Price

- Back Taxes and other liens

- Contractor or do it yourself

- Payments on hard money loan

- Other non-related expenses

2. Have a good team of Contractors/others to do the work.

- Real Estate Agent (hopefully it will be you)

3. Get educated.

Don’t start buying homes without knowing the process. The best way to get started is to get your Real Estate license. Yes, it’s work, but it will give you the knowledge you need to understand how homes are transferred and the laws associated with real estate. Also, you will have access to the multiple listing service, which is invaluable for your research. Plus you can avoid the partial cost of the seller commission since you will be the listing agent. Every successful flipper I’ve ever meet had their real estate license.

4. Be patient.

There used to be a lot of homes being sold on the court room steps, sometimes a 1,000 homes per day. Today there are a lot less homes to purchase. You need to look at other ways of purchasing and finding deals. It’s going to take time to find, fix and sell. You can do it, but it’s going to take time. In the real estate investment world, timing is everything.

5. Have Money.

Don’t believe those people on the radio that say you can buy homes for no cash down. It’s not true.

You are going to have to have cash, skin in the game to purchase the home. Private hard money will require a down payment of 20-30% of the purchase price. And it’s not going to be cheap when you start. Rates vary from 9-18%. Don’t forget to calculate the cost of Hard Money in your profit and loss in item 1 above. Some hard money lenders market their loans as having the potential to fund an investment at 100% LTC (Loan-To-Cost), meaning a borrower won’t have to put a dime into the project. Although there are some scenarios where this is true, it’s very rare. There are some lenders that will participate in the deal. These lenders will fund the deal and share in the profit when the deal is completed. However, all of the participating lenders put a great deal of their decision on working with you on your response to #3 above and still require 10% of your money in the deal.

6. Don’t buy something you can’t fix or ever sell.

There are a lot of deals out there and they are deals for a reason. Some are in a situation, so bad, no matter how much money and work you put into the home, you will never sell it. For example a home built on top a land fill, or next to a dump, or sewage treatment facility, or the final approach to an major airport. You are not going to be able to fix these problems.

7. Buy your project through your LLC.

There is a lot of tax and liability reasons to do this. Plus, private lenders prefer to lend to LLCs.

8. It’s going to be work.

Don’t believe what you see on those flipping shows. You will have to work at it and it will take time. You need to visit the property and make sure the work is progressing correctly. After the home is completed and on the market, you will need to walk the property daily. So where do you start? I suggest that you start with #3 Get Educated. However, don’t go and pay for those weekend training seminars that cost 1,000s of dollars. Start at your local Real Estate School and get your State License.

About ME.

Hi, my name is Dennis Love.

I’m a business owner like you with over 40 years of business experience helping business owners around the world, including 7-figure businesses, small businesses and startup businesses that now make millions of dollars per year.

But the question is why do I do this? Personally, I had a very special person do something for me in the past to help me in my life. That person help me to grow to be the best that I could possibly be. This person sacrificed everything to help me to the point that in their efforts they died for me. It’s hard to understand this amount of sacrifice. It’s hard to swallow, but I learned from sacrifice of this special person that living is not taking but that in giving to others is when you really achieve true purpose and happiness. That’s why I do this. I want to be of service to you so you can achieve the dreams, success and happiness that you long for in your business.

Servicing others is the true wealth and the path for happiness. When you are successful, I’m successful. So with that let me tell you about my recent struggles.

I have personally helped business owners who were on the verge of going out of business to making a profit in as little as a few weeks.

But you want to know something interesting? Just a few years ago my wife and I were homeless and living in the van and sleeping in the office. That’s true! After 30 years my business was failing and I was laying off 100’s of employees. I was losing $250,000 per month and was going down in flaming colors. The only cash I had remaining was the credit line on my credit card, and after I maxed this out I had nothing but the van and luckily a wife who still had faith in me. Creditors were calling; I was being sued and hauled into court to stand before the judge subject to debtor exams. I had judgments filed against me, and creditors coming to the office and seizing assets. I tried everything but nothing worked. I just kept going losing money, more money and more money --- till it was all gone. I lost my business, cars, airplane, and even the home I was living in.

Everything gone!

No matter how hard I tried flipping homes, even though I worked 14 hours per day, nothing was working. I was so stressed that I ground down my teeth down and cracked every tooth. I had to find another way of making money flipping homes that would not cost me 1000’s of dollars. I could no longer spend thousands of dollars which I no longer had, on the old school approach that that cost 1000’s had returned nothing.

Finally late one night I found myself sitting on the edge of the bed with a gun in my hand and the memories’ of the business past. Than I had an awakening.

I heard a voice that said “what you think and feel is not reality; flipping homes is not brain surgery; it really is easy; you can do it.”

How hard can it be!

You just need to get educated and find out how other companies are making money flipping homes.

So after many failures I figured it out. I wrote this basic guide to help you. Servicing others is the true wealth and the path for happiness. When you are successful, I’m successful.

![Level-4-Funding-Dennis-Dahlberg-Mort[1]](https://blogger.googleusercontent.com/img/b/R29vZ2xl/AVvXsEjjY0RQ4LcV1QiDROz3SqiBuRmQJppi0FFUwC99Keo7gTLyXL2PMFN68yMSxmyQNk_1HHf5US-KWS3bGDBHQrkYMzCMiqMNw4M3C-lAB8d69DeOlmwamWOAg7-Y4h2bxOEBCv9fJe-ak-Q//?imgmax=800 "Level-4-Funding-Dennis-Dahlberg-Mort[1]") Dennis Dahlberg Broker/RI/CEO/MLO

Dennis Dahlberg Broker/RI/CEO/MLO

Level 4 Funding LLC

Arizona Tel: (623) 582-4444

Texas Tel: (512) 516-1177

Dennis@level4funding.com

www.Level4Funding.com

NMLS 1057378 | AZMB 0923961 | MLO 1057378

22601 N 19th Ave Suite 112 | Phoenix | AZ | 85027

111 Congress Ave |Austin | Texas | 78701

About the author: Dennis has been working in the real estate industry in some capacity for the last 40 years. He purchased his first property when he was just 18 years old. He quickly learned about the amazing investment opportunities provided by trust deed investing and hard money loans. His desire to help others make money in real estate investing led him to specialize in alternative funding for real estate investors who may have trouble getting a traditional bank loan. Dennis is passionate about alternative funding sources and sharing his knowledge with others to help make their dreams come true. Dennis has been married to his wonderful wife for 40 years. They have 2 beautiful daughters 5 amazing grandchildren. Dennis has been an Arizona resident for the past 38 years.

Dennis Love, DennisLove.com are spoke persons or trademarks of Lever 4 Funding LLC an Arizona Limited Liability Company. This is for educational purposes and you should contact competent individuals such as Attorneys, CPA, Real Estate Brokers for expert advice. Information presented is not considered accurate and complete. To the extent this message includes any tax or legal

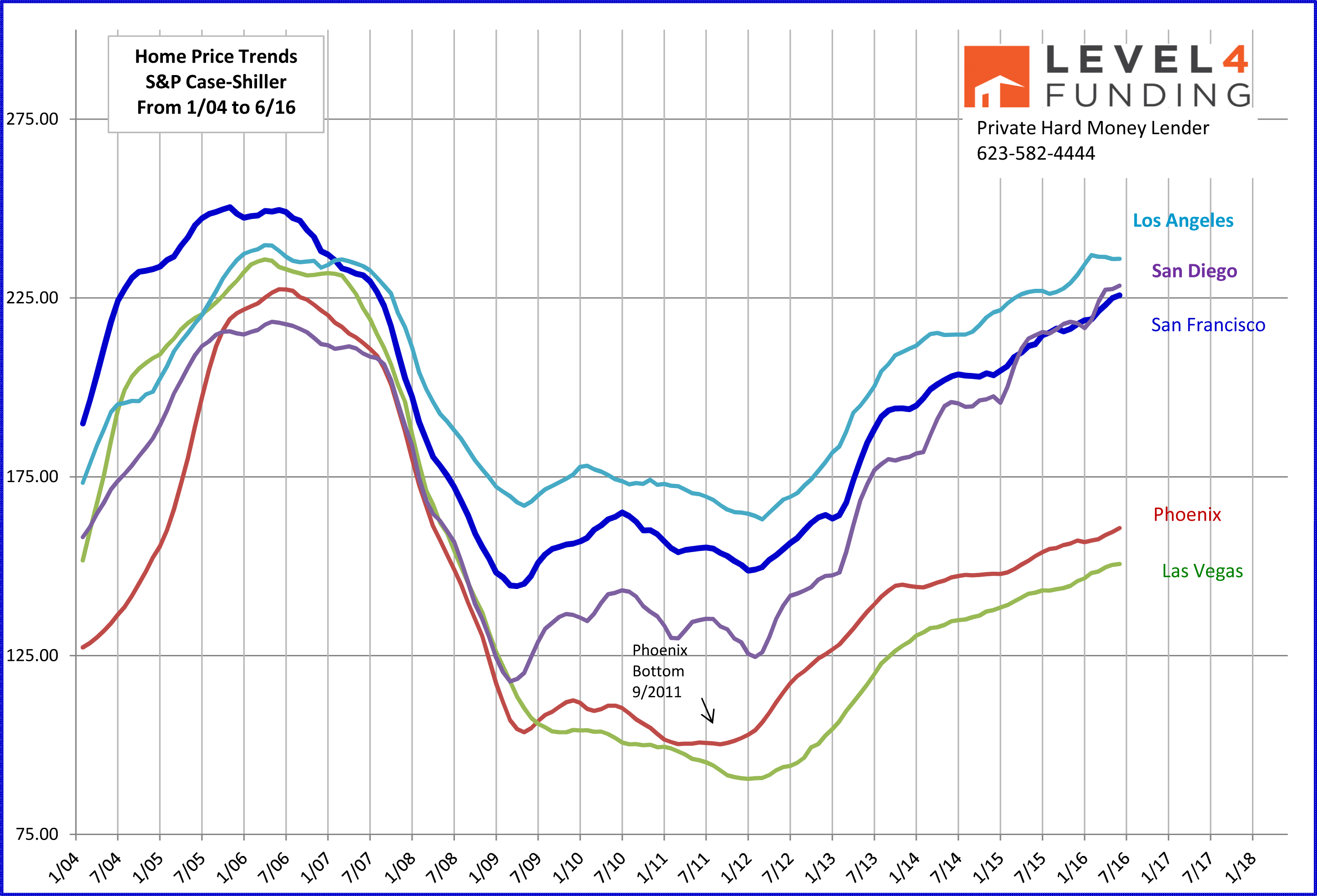

For Phoenix the bottom was officially September 2011.

For Phoenix the bottom was officially September 2011.![Level-4-Funding-Dennis-Dahlberg-Mort[1]](https://blogger.googleusercontent.com/img/b/R29vZ2xl/AVvXsEg56lEEdhF5RxMWm3UPS4zDV9gTX_EJU0U4k7xzoXgVwJ7V0GGS-H3cZV0LFSZC3TjccR0iIxwgNgh9-Tfjo0hcB-WTurHnbZ63-bwe6cvqCNLBsnz3yhQaK7JpttovAkj_Ob3Wmg5ji0pc/?imgmax=800 "Level-4-Funding-Dennis-Dahlberg-Mort[1]")

Dennis Dahlberg

Dennis Dahlberg